Transaction scoring offers the most significant enhancement to data-driven risk management since the introduction of Comprehensive Credit Reporting. illion CEO Simon Bligh outlines how credit risk management is improved through the implementation of transaction scoring.

Financial institutions hold a raft of data that shows both the financial state and spending behaviour of a depositor. This information is captured whenever there is an inflow or outflow of funds in a current account, overdraft, credit card, revolving personal loan or home loan.

While this data offers the capability to understand consumer spending behaviour, most financial institutions have made limited use of it for this purpose. For example, it has rarely been used to understand a consumer’s propensity to modify consumption habits in-line with their economic wellbeing.

Furthermore, by their nature, smaller banks have traditionally had limited access to transaction information, as they generally have held a secondary relationship with the consumer. This has disadvantaged them when competing with tier 1 banking institutions for prime borrowers.

Developing a transaction score

By providing fresh and unique insights into consumer behaviour, both lenders and consumers stand to profit significantly through better credit underwriting, more effective loan pricing and more tailored lending terms and conditions. This great step-change to the credit landscape can be achieved through transaction scoring, where a consumer’s income and expense transactions are used to generate a score that summarises the consumer’s cashflow patterns.

Developing Transaction Scores requires both a technical understanding of banking data structures as well as a deep knowledge of spending and broader consumption behaviour. Transaction scores require highly complex data processing and modelling to achieve an optimal outcome. illion coded and analysed more than 1,000 business-interpretable transaction data features, then used a combination of traditional modelling and Machine Learning techniques to develop the illion Transaction Risk Scores.

Complex features we looked at include buy now pay later usage, rate and size of cash withdrawals and consistency of bill payments.

illion Transaction Risk Score Launch

Join us for an evening where we unveil New Zealand’s most predictive new credit risk assessment service, and discuss how transaction risk scoring can lead to better outcomes for your business.

Amazing benefits

In a case study of a Personal Loan provider, a 7.3-Gini-point uplift was achieved by blending illion’s Transaction Score with the lender’s own application scorecard, resulting in a Gini gain from 50.7% to 58.0%, which could allow them to fund more loans for the same level of risk. Gini is a statistical measure of how well a credit rating can predict consumers’ future credit repayments.

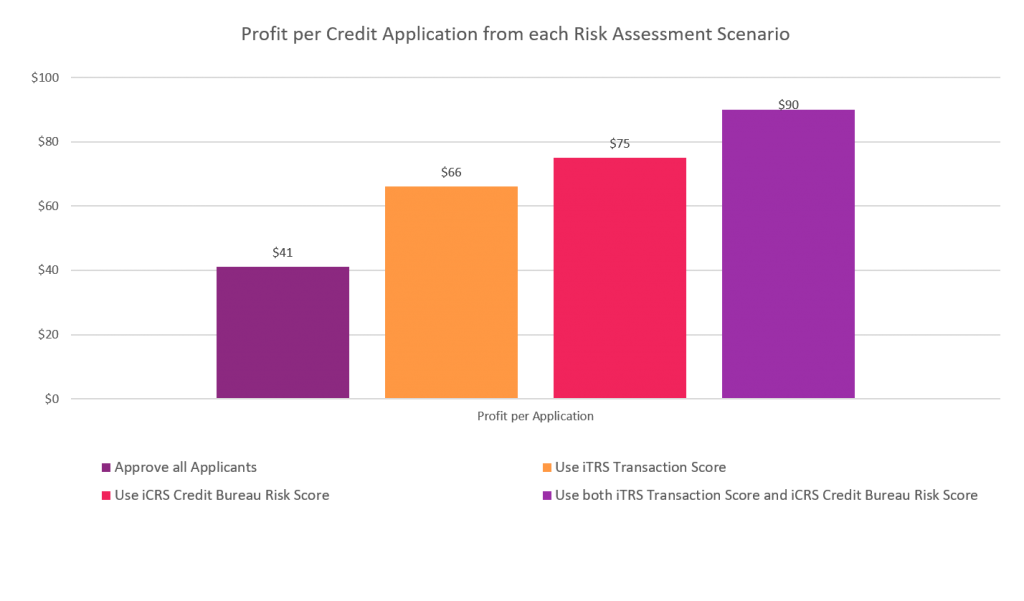

When assessing the business benefits of utilising the illion Transaction Risk Score (iTRS), analysis uncovered that it is in fact highly beneficial for credit providers to leverage the transaction score in conjunction with the illion Consumer Risk Score (iCRS), which is illion’s flagship consumer credit rating. You can check your own iCRS through CreditSimple.co.nz

For this credit provider, they could increase profit per application from $41 to $66 by enriching their underwriting with the illion Transaction Risk Score. Use of the illion Consumer Risk Score would allow the credit provider to unlock $75 per application, while using both scores together could unlock $90 profit per application.

The inclusion of transaction data could increase portfolio profit by a further 20% over traditional credit risk data alone. This incremental benefit is especially important to realise in periods of tighter lending and riskier credit, which may be the norm in 2021.

Off the shelf or DIY?

Some credit providers have recognised that integrating transaction data as part of their risk strategy would add powerful insight into their risk assessment capability. However, many of them did not understand the complexity of building and implementing a transaction scoring capability, sometimes aborting these initiatives prior to completion.

Feedback to illion has shown that while credit providers generally saw strong benefits from transaction scoring, they often concluded that its implementation cost and project failure risk made the ‘in-house’ development of these scores unviable. In some cases, this may have been due to a lack of in-house modelling expertise or to limitations in their ability to identify, maintain, and implement transaction-based features in both analytic and real-time environments.

Obtaining the benefit from modelling customer behaviour has traditionally necessitated significant investment in systems and processes. Typical projects have rarely been delivered in less than 18-24 months and have mostly come with a multi-million-dollar investment cost. Furthermore, as transaction data analysis evolves into the future, significant ongoing investment would be required to stay competitive in market.

illion Transaction Risk Score Launch

Join us for an evening where we unveil New Zealand’s most predictive new credit risk assessment service, and discuss how transaction risk scoring can lead to better outcomes for your business.

illion’s solution

illion has a market-leading position in bank transaction categorisation, risk analytics and bureau services, meaning that it is ideally placed to develop a scalable Transaction Scoring service that is economically viable for all credit providers.

The illion Transaction Risk Scores are built using many of the same robust analytical techniques that are used in illion’s consumer credit ratings. The features that drive the iTRS have been hand-crafted using over one billion banking transactions from over 2.5 million consumers and 160 institutions.

Furthermore, the iTRS factors in a wide range of consumer transaction behaviours that have each been scrutinised by credit experts to ensure such trends will continue to be robust into the future. The combination of these factors can allow credit providers to trust illion’s Transaction Risk Scores to drive immediately improved customer outcomes and significant business value.

By using transaction data as part of a risk strategy, most notably through the consumption of transaction scores, we believe that credit providers will be able to set a clear path for the integration of transaction scoring into their risk assessment process.

Don’t wait until 2022+ to begin benefiting from this innovation; through the use of iTRS, illion can support credit providers to start extracting the value of iTRS before 2021 is complete.